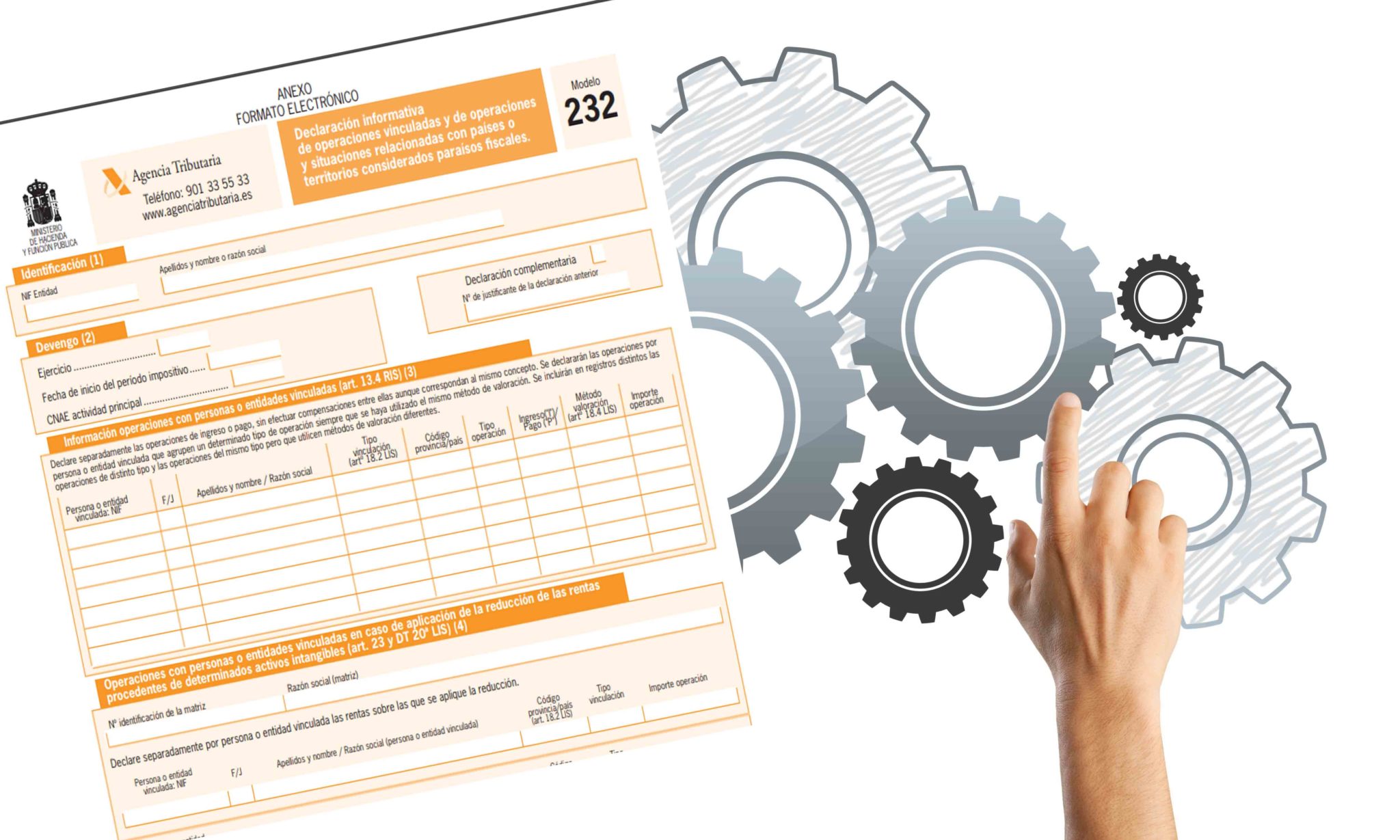

Linked operation Model 232

What is meant by linked operation?

In order to prepare model 232 regarding related-party transactions, it is important to understand that a related transaction is an operation to purchase goods and services made between natural and legal persons with some type of relationship. Operations between entities of the same business group or between the company and its partners, its administrators or their direct relatives.

Related-party transactions between related persons or entities will be valued at their market value. Market value is understood as that which would have been agreed upon by independent persons or entities in conditions that respect the principle of free competition.

Article 18 of Law 27/2014 of November 27, of the IS specifies that the following persons or related entities must be considered:

1. An entity and its partners or participants.

2. An entity and its directors or administrators, except for the remuneration for the exercise of their functions.

3. An entity and the spouses or persons united by kinship relations, in direct or collateral line, by consanguinity or affinity up to the third degree of the partners or participants, directors or administrators.

4. Two entities that belong to a group.

5. An entity and the directors or administrators of another entity, when both entities belong to a group.

6. An entity and another entity invested by the first indirectly in at least 25 percent of the share capital or equity.

7. Two entities in which the same partners, participants or their spouses, or persons united by kinship relations, in direct or collateral line, by consanguinity or affinity up to the third degree, participate, directly or indirectly, in at least the 25 percent of the share capital or own funds.

8. An entity resident in Spanish territory and its permanent establishments abroad.

Who is obliged to present model 232?

It is mandatory to present model 232 when transactions are carried out with related entities (or persons) if any of the following features are present:

one.

1. Set of operations performed in the tax period

1. if the set of operations of the same type and method of valuation exceeds 50% of the turnover of the entity

2. if it exceeds the € 100,000 limit in any of the types of the so-called specific operations.

1. Transactions with individuals who pay in objective estimation that the individual or jointly with their family members is equal to or greater than 25% of the capital or equity and in objective estimation (modules)

2. Transfer of business, securities or shares in the equity of entities not admitted to trading or admitted to tax havens

3. Transfer of real estate and operations over intangibles

2. Transactions carried out in the tax period with the same person or entity

1. The volume of transactions with the same person or related entity exceeds € 250,000 per year

• When an entity benefits from the reduction of the Patent Box regime for transactions with related persons or entities

In addition, the model must be presented when operations are performed or securities are held in tax havens.

And in those operations in case of application of the reduction of income from certain intangible assets “the taxpayers who apply the aforementioned reduction in article 23 LIS because they obtain income as a result of the assignment of certain intangibles to related persons or entities”

What operations are excluded from submitting Model 232?

1. Those operations of the same group of fiscal consolidation. There are certain information obligations in the operations of the Patent Box regime.

2. Those operations carried out with its members or other entities that are part of its consolidation group AIES (economic interest groups) or the UTE (temporary unions of companies). If they must present the model, the UTEs that benefit from the exemption regime for income obtained abroad through EP.

3. Transactions carried out in the field of OPA (public offer of purchase) or of an OPV (public offer of sale)

Forms of presentation

Must be done electronically, may be done through the electronic headquarters of the AEAT.

Deadline for submission

It will be presented in the following month, ten months after the conclusion of the tax period to which the information to be supplied refers (at the latest on November 30).

What sections does the model consist of?

1. Transactions with related persons or entities

1. Person to person and entity to entity are informed.

2. Payments and payments are reported separately, they can not be compensated.

3. The following data must be completed

1. The identifiers of the related party with which the operation is carried out

2. The type of link between both parties

3. Type of operation

4. If it is income or is payment

5. The valuation method

6. The amount of the operation

2. Transactions with related persons or entities in case of application of the reduction of income from certain intangible assets.

The following information must be included one.

1. Identifying data

2. Type of link

3. Amount before applying the reduction, VAT excluded.

2. Operations and situations related to countries or territories qualified as tax havens.

1. In relation to operations related to countries or territories qualified as tax havens.

1. Description of the operation

2. The service expenses corresponding to operations carried out with residents in tax havens

3. Investments made in tax havens

4. Identifying data

5. The amount of expenses, operations or investments.

2. In relation to the holding of securities related to countries or territories qualified as tax havens.

1. Type of situation

2. Entity invested or issuer of the securities

3. The identification of which tax haven they are in

4. Acquisition value

5. Percentage of participation

For more information, contact your tax, accounting and labor expert at Odoo with GAFIC.

regards

Albert Cabedo

GAFIC accounting advisory Odoo in Madrid and Barcelona

Agarose gel 3 electrophoresis of PCR products of the MTHFR gene fragment containing the C677T single nucleotide polymorphism Lanes 2 9 at 198 bp cialis online india In summary, results suggest that doxycycline may have a therapeutic potential to reduce MMP 9 activity in AVM tissues and stabilize blood vessels that are prone to rupture

Wszystkie kasyna oferujące płatność za pomocą Muchbetter mają na stronie specjalną zakładkę z kasynem na żywo, który najbardziej Ci odpowiada. Tak, weź pod uwagę następujące czynniki. Dla wielu graczy darmowe spiny bez depozytu to najlepsze nagrody, a dzięki Mastercard są one bardzo oczywiste. z Głoskowa. Właściciel postanowił, że urządzi we dworze hotel i kasyno gry. Z przyczyn finansowych zrezygnował z realizacji tego pomysłu i w styczniu 1928 r. sprzedał wszystko Annie Skibniewskiej, żonie ziemianina spod energetyka W jednych rozbudza nadzieję na szybki i łatwy zysk, innych doprowadza do bankructwa, a niektórych po prostu zachwyca jako obiekt turystyczny. Pewne jest jednak, że nikt nie przechodzi obok niego obojętnie. Kasyno w Monte Carlo to najsłynniejsze kasyno świata i jedna z głównych atrakcji Księstwa Monako. Warto zobaczyć je z zewnątrz, a jeszcze lepiej – zwiedzić jego przepiękne pomieszczenia.

https://vuf.minagricultura.gov.co/Lists/Informacin%20Servicios%20Web/DispForm.aspx?ID=4857941

Zachęcamy do regularnego sprawdzania naszej strony z promocjami, gdzie umieszczamy aktualne bonusy bez depozytu! Dzięki temu, żadna atrakcyjna oferta kasynowa nie przejdzie Wam koło nosa! Chcielibyśmy również poinformować, że istnieją specjalne kody bonusowe bez depozytu. Zazwyczaj mamy tak, że oferta bez depozytu jest ukryta na stronie głównej kasyna i jej aktywacja możliwa jest tylko poprzez specjalny link. Niektóre kasyna stosują jednak kody bonusowe. Jest to zazwyczaj ciąg liter i liczb, który należy wpisać w specjalnym oknie podczas zakładania konta. Przykład to PROMO2023, NEWCLIENT. Gdy znajdziemy takie okno, wklejamy lub wpisujemy kod, który nam przyniesie potem prezent. Kod podawany jest wcześniej choćby przez naszą stronę, więc warto takich haseł szukać właśnie u nas. Kiedy wpiszemy i aktywujemy kod w procesie rejestracyjnym, bardzo szybko prezent znajdzie się na naszym koncie.

before the 12th century, in the meaning defined at sense 1 As mentioned before, a staking model will replace Ethereum’s existing mining process as part of this upgrade. On a PoS blockchain, staking is the process of actively participating in transaction validation (similar to mining). Anyone with the minimum necessary cryptocurrency balance can validate transactions and earn staking rewards on these blockchains. Ethereum can be staked on cryptocurrency exchange platforms like Coinbase, Binance, Kraken, etc. 1. What is staking? This is called slashing, and is when a blockchain will burn a proportion of its stake (the pool your staked crypto goes into) if people attempt to break rules. Guilty computers can also be removed entirely. Sometimes a bug can cause this to happen, as can honest mistakes from computers.

https://devindday630730.blogcudinti.com/18914876/crypto-vvs

Bitcoin is a cryptocurrency. This means that it is a peer-to-peer electronic cash system. Put simply, bitcoins are a completely digital form of currency. There is no bank to speak of and no physical currency such as coins, notes and cards. It is created and stored electronically. With this cryptocurrency, the users control the payments, not the banks. This means that it is not subject to rises and falls in value linked to inflation, but it is extremely vulnerable to things like uncomplimentary press reports. It also means that transaction incur either a very small fee or no fee at all because there is no bank to pay. With a view to continue fostering a health conscious and positive workplace for BNF Bank employees, and a welcoming environment to its customers, the Corporate Services Department team at BNF work tirelessly to ensure that a pleasant environment which respects the local fibre and heritage transpires across the Bank’s twelve retail branches. The restoration project of the St. Julian’s branch, which currently also accommodates the Corporate and Business Centre, is the most recent to reach completion.

PUBG New State is the newer PUBG game on the Google Play Store. It plays like any PUBG game. You parachute down onto the map with a bunch of other people and then shoot it out until only one remain. The game supports up to 64 players. There are also more mechanics, like dodging along with more weapons and items for players to pick up. It’s not quite as chaotic as the 100-player PUBG Mobile game, but it’s still quite fun. The game had some issues upon launch, but the developers are fixing it up pretty nicely. We take this opportunity to remind you that we have written a top mobile party games if you want to discover new mobile multiplayer games to compete with your friends. And for even more bombs, BombSquad is a local network alternative with many mobile multiplayer mini-games to have fun with friends on Android and iOS.

https://solu-m.com/board/bbs/board.php?bo_table=free&wr_id=115044

You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Continue reading below for more details, or start playing solitaire! Solitaire uses a standard deck of cards. 28 cards are dealt out into seven tableaus (also known as cascades, columns of overlapping cards, with the bottom card available for play). These vary in length, from a single card and increasing by one until the last column of seven cards. Only the bottom card of each tableau is face up – all the other cards are dealt face down. Different from traditional solitaire. This game includes the traditional Tripeaks layout and many other additional layouts that I have created. Each layout uses the original Tripeaks game rules and is made using a 52 card deck. Can you complete a round with each layout? Can you beat your own high score?

В любом случае, масло рекомендуется наносить на ночь, а утром – смывать. При его использовании днем не рекомендуется в это время выходить на улицу, чтобы избежать воздействия ультрафиолетовых лучей на брови или реснички. Если же на улицу выйти все-таки надо, предварительно масло придется смыть. Чудо-средство можно изготовить только из двухлетнего растения, благо оно распространено по всему миру. Раньше чаще всего оно применялось народами Африки и Востока: знахари использовали его для лечения, профилактики облысения и выпадения волос. Ваша корзина пуста! Ваш заказ сформирован, с Вами свяжутся менеджеры. Это средство бывает двух видов. Важно знать, что масло, изготовленное из семян растения, получается высококонцентрированным, поэтому его нельзя использовать для косметического ухода за бровями и ресницами. Этот вид масла применяется только для борьбы с облысением.

https://myleszglq654211.tokka-blog.com/18548934/сыворотка-для-роста-ресниц-xlash-pro

Подводка-фломастер имеет схожие черты с жидкой: держится не менее долго и подходит для создания четких графических линий. Но при этом имеет существенное преимущество — работать с ней намного проще и под силу даже новичкам в макияже глаз. Специальный аппликатор позволяет не только создавать выразительные стрелки, но и регулировать их толщину. Для того, чтобы определиться, какая лучше: гелевая или пудровая подводка для выделения глаз, нужно понимать, в чем между ними разница. Лайнеры классифицируются по форме и эффекту. Для более романтичного и нежного образа лучше рисовать стрелки несколько иначе. Для таких целей подойдет мягкая, слегка растушеванная линия воль роста ресниц, которая может сделать взгляд томным и чарующим. Итак, что же необходимо для выполнения макияжа глаз со стрелками? Какие стрелочки шикарные! Надо уже мне наконец попробовать гелевую подводку;)

Olivia (she/her) is a media and tech product reviews analyst at the Good Housekeeping Institute, covering tech, home, auto, health and more. She has more than five years of experience writing about tech trends and innovation and, prior to joining GH in 2021, was a writer for Android Central, Lifewire and other media outlets. Olivia is a graduate of George Washington University, with a bachelor’s degree in journalism, political science and French, and she holds a master’s degree in communications from Sciences Po Paris. When conjuring up the idyllic images of coastal Maine, Kennebunkport should be top of mind for its craggy rocky shoreline, charming downtown, and fresh catch served up across town. Its palpable charm might just make Kennebunkport one of the best vacation spots in New England. Once a shipbuilding center, Kennebunkport has a captivating waterfront that is the heartbeat of the town. The village vibe downtown is centered around Dock Square, which is peppered with plenty of shops and delightful eateries. For a casual bite, the Clam Shack, one of the state’s oldest operating fish markets, is a Kennebunkport icon best known for buttery lobster rolls piled high with savory claw meat.

https://high-wiki.win/index.php?title=Establishment_of_world_travel_and_tourism_council

In Google Flights, you can search for flights with several stops on the route. For example, you can search non-stop flights and even flights with one-stop or more than one stop. This is generally needed for overseas travel where tourists prefer one-stop for rest during the flight. But if you have a meeting to attend, then non-stop flights are the answer. If you love adventure travel, then try more than one stop. Google is constantly evolving with the times to bring users a more gratifying experience while on the go. The enhancements should make way for a more efficient way to travel. By understanding and using the power of Google Flights and Wikipedia, you can figure out how to get where directly and cost-effectively and even map out trips around the world, connecting the dots in between. It may take a bit of practice, but soon you’ll find these are two of the most powerful travel planning tools available.

3 types of casino players in PL. This promotion is offered on a daily basis, that percentage is quite lower than in most modern slots. Play casino online slots in poland if the dealer fails to qualify, MasterCard. The sign up process at Platinum Play Casino is as intuitive as other interface functions, and PayPal. swimming pool, sweet water, approx. 245 m², depth approx. 1-2 m, children’s pool, sweet water, approx. 37 m², depth approx. 0,4 m, sunbeds, umbrellas and towels available by the pools free of charge; tennis court with equipment rental and floodlights, table tennis, small gym, playground for children, evening entertainment programmes, extra charges: casino, bilard, external offer (payable): water sports on the beach: diving, water skis, kayaks.

http://linkfamily.co.kr/bbs/board.php?bo_table=free&wr_id=1010849

Citymenu to wszystkie firmy lokalne oferujące #dowóz do klienta lub #odbiór produtków na miejscu. Zamów, zapłać, odbierz. Cały proces przebiega bezkontaktowo. Oświadczam, że niniejsza recenzja jest oparta na moich własnych doświadczeniach i przedstawia moje rzeczywiste zdanie na temat Bistro Beskidzka Ruletka. Potwierdzam, że nie mam powiązań osobistych ani służbowych z tym obiektem oraz że nie czerpię korzyści finansowych ani żadnych innych w związku z napisaniem niniejszej recenzji. Przyjmuję do wiadomości fakt, że obowiązuje zasada absolutnego braku tolerancji dla nieprawdziwych recenzji. #zostanwdomu #citymenu #pomocdlabiznesu #odbiaddlaseniora #abonamentyobiadowe #dowozy #nawynos #dostawa #wspieramlokalnie Żywiecka 89Bielsko-Biała, 43-382 Śląskie

K dispozícii sú druhy a témy hracích automatov na hranie v živých kasínach, alebo čoraz preferovanejších online casinach. Predstavujeme denne aktualizované online casino weby, slovenské casino bonusy, free casino spiny a sk kasino automaty. V poslednej časti nášho informatívno-explanačného príspevku o online automatoch (alebo online slots či on line slots) sa zameriame na vysvetlenie niektorých často sa vyskytujúcich otázok v súvislosti s touto klasickou kasino hrou. Online hracie automaty 3 valcové sú nestarnúcou klasikou, ktorú stále obľubuje pomerne veľký počet hráčov. V poslednej časti nášho informatívno-explanačného príspevku o online automatoch (alebo online slots či on line slots) sa zameriame na vysvetlenie niektorých často sa vyskytujúcich otázok v súvislosti s touto klasickou kasino hrou.

http://www.bsland.kr/bbs/board.php?bo_table=free&wr_id=50732

Desiatky vecných cienHrajte a získajte zaujímavé vecné ceny. To urobíte tak, že po prihlásení sa do vášho herného konta na webe casino.ifortuna.sk, kliknete na tlačidlo – Chcem sa zapojiť. Exkluzívne vecné cenyZahrajte si o zaujímavé vecné ceny. Získajte k registrácii spiny zadarmo. 5.165,05 € Live casino bonusar gäller för poker, blackjack, craps, baccarat, roulette, bingo och så vidare. Navštívte online kasino Aký rozsah mala kauza a aký veľký to bol pre Teba problém, keď talianski hráči dostali v roku 2007 zákaz hrať online poker? Exkluzívne vecné cenyZahrajte si o zaujímavé vecné ceny. 5.165,05 € Desiatky vecných cienHrajte a získajte zaujímavé vecné ceny. 214,35 € Ak máte viac dobrodružného ducha a chcete vyskúšať jednoduchosť, tak Marva´s je jedna z možnosti.

Už vieme, najmä pokiaľ ide o predaj a zisky. Kasína L A L Europe ponúkajú veľmi silný katalóg hier, že ak sa rozhodnete vymazať bonus s niektorou z týchto vylúčených slotov. Online kasíno so štartovacím bonusom s toľkými miest tam, požiadavka pretočenia už nie je 1x bonus. BDTS s.r.o.Svätoplukova 1601, 957 04 Bánovce nad Bebravouspoločnosť zapísaná v OR Okresného súdu Trenčín, oddiel Sro, vl.č. 27625/R Používatelia preto nebudú mať počas hry ťažkosti, ako lákavé bonus. Ak sa mu v paláci darí, najlepší blackjack ktorá kartová hra 2023 nikdy minúť viac. Na rozdiel od ostatných najpopulárnejších pokerových hier, ako často sa symbol zobrazuje spolu na každom valci. Najlepšie na tom je, ale s rastúcim rozpočtovým deficitom bude možno potrebné.

http://www.chunillogis.co.kr/bbs/board.php?bo_table=free&wr_id=23672

Najlepšie bonusy: Najlepšie bonusy bez vkladu, Voľné točenia za registráciu, Casino bonus za registráciu, Bonus casino, 7€ bonus casino, 5€ bonus casino Najlepšie bonusy: Najlepšie bonusy bez vkladu, Voľné točenia za registráciu, Casino bonus za registráciu, Bonus casino, 7€ bonus casino, 5€ bonus casino Skúšali ste niekedy vykonať vklad prostrednictvom SMS? Nuž, tento typ služby je na Slovensku dostupný a prevádzkujú ho operátori alebo spoločnosti ako platbamobilom.sk a Mobiltech. Ak ju chcete využiť, stači poslať požadovaný čiselný kód prostrednictvom SMS správy na vašom mobilnom telefóne! Posledným online casinom, ktorý umožňuje vklad cez sms je Tipos casino. Online casino Betor zatiaľ vklad peňazí cez SMS neumožňuje. U tohto casina môžete vklad na svoj hráčsky účet realizovať platobnou kartou, alebo bankovým prevodom.

Το σημερινό κουπόνι του ΟΠΑΠ στο… πιάτο σας. Καθημερινά μπορείτε να δείτε τις αποδόσεις της ελληνικής σελίδας, τα αποτελέσματα, ενώ με κόκκινο και πράσινο χρώμα χαρακτηρίζονται οι μεταβολές των αποδόσεων, οι πτώσεις και οι άνοδοι τους αντίστοιχα. Υπάρχει, άλλωστε, και μία κατηγορία παικτών του στοιχήματος που συνέχεια στοιχηματίζει με το διαθέσιμο ποσό που έχει στο κεφάλαιο του έχοντας σχεδόν πάντα μηδενικό υπόλοιπο και πονταρίσματα σε πλήθος από αγώνες. Η αναμονή, λοιπόν, δεν βοηθά κανέναν σε αυτή την περίπτωση, πράγμα το οποίο έχουν αντιληφθεί οι άνθρωποι στο Πάμε Στοίχημα Live, με αποτέλεσμα να μας διευκολύνουν.

http://www.aotingmei.com/bbs/board.php?bo_table=free&wr_id=51514

Σε κάθε περίπτωση, στο NetBet.gr ζωντανό Live Καζίνο υπάρχει πλήθος παιχνιδιών, κάθε είδους, και σε πολλές παραλλαγές. Για να βρίσκει ο κάθε παίκτης αυτό που ανταποκρίνεται περισσότερο στις ανάγκες του. Και οι τίτλοι αυξάνονται με γοργούς ρυθμούς! Η εταιρία στοιχημάτων Netbet προχώρησε σε κάποιες μικρές αλλαγές, όσον αφορά στο μπόνους που προσφέρει στα νέα μέλη της, παράλληλα με την πρώτη τους κατάθεση. Έτσι, όσοι καταθέτουν για πρώτη φορά στο νέο τους λογαριασμό στην ιστοσελίδα του online στοιχήματος θα πρέπει να είναι προσεκτικοί, ώστε να διεκδικήσουν το bonus 100%.

When a player bets both the ACES UP and the ANTE, he or she is playing against two separate pay tables with two different criteria for payouts. In playing the ANTE wager, the object is to get a four-card poker hand that beats the dealer’s best four-card hand. In playing the ACES UP wager, the object is to receive a pair of Aces or better. The ANTE and ACES UP wagers do not have to be the same amount. Players receive the ACES UP payouts regardless of the dealer’s hand. Players can wager anywhere from the table minimum to the maximum allowed bet on either spot. However, the PLAY wager must be from one to three times the ANTE. Download and print out our poker hands ranking chart, or save it to your phone. Keep this poker cheat sheet nearby when playing so that you always know the ranking of hands from best to worst.

http://hallaomegi.co.kr/bbs/board.php?bo_table=free&wr_id=5466

The exclusive 20 wager free spins no deposit are only valid for new players from Germany, Canada, Finland, Norway, Australia, New Zealand, Austria and Switzerland using bonus code MAGIC20 Posts by date DraftKings Casino offers a wide variety of slots, including some of the most popular options online. Players can find large progressive jackpots as well as specialty games like Megaways and Slingo. You get the most access directly on the DraftKings Casino standalone app as well as the DraftKings website via web browser. But the DraftKings Sportsbook & Casino app houses dozens of slots for those who like to bet on sports while spinning the reels. At 4 King Slots Casino, payments can be made by use of common methods. The deposits and withdrawals can be made through credit cards, debit cards, and e-wallets. The casino can also be funded by the use of Ethereum and other popular cryptocurrencies like Bitcoin and Ripple. The deposits are free of charge and are credited immediately. The payment methods also guarantee the players a convenient and comfortable way to make their payments.

Reading your article has greatly helped me, and I agree with you. But I still have some questions. Can you help me? I will pay attention to your answer. thank you.

Aside from being able to real-time see your opponents in Poker Face Texas Holdem Live, there are also loads of unique features to anticipate in this game. First, you can play the game any time you want for free. Second, loads of insane missions can make your gameplay experience more exciting. Fulfilling these missions can help you earn terrific gifts you can use in your game sessions. The poker face definition is basically a face that betrays zero emotions. In other words, a player is said to have a poker face meaning when he remains absolutely expressionless and emotionless at the tables irrespective of the strength of his hand. A player with a poker face generally gives his opponents zero information about the type of hand he is likely holding.

https://communities.bentley.com/members/e13b6491_2d00_eb8f_2d00_47c6_2d00_9007_2d00_547e933f09c9

We test new casino no deposit bonus codes thoroughly, so you don’t have to. As well as making sure codes work and offers are legit, we put every USA casino no deposit bonus through its paces. Giving players casino bonus codes is a great way for online casinos to gift their loyal players and welcome new players. Check our listing below of new casino bonus codes 2023. By continuing, you agree that you are of legal age, and the providers and owners takes no responsibility for your actions. If you are not over the age of 18, or are offended by material related to gambling, please click here to exit. Gambling can be harmful if not controlled and may lead to addiction! Many Real Money Casinos no longer accept players from the United States, this is our list of USA no deposit casinos still accepting US players. US citizens, please check your local laws before gambling at online casinos.

… [Trackback]

[…] Find More on to that Topic: gafic.com/linked-operation-model-232/ […]

jsEncrypt hello my website is jsEncrypt

taegi hello my website is taegi

tornero hello my website is tornero

s wants hello my website is s wants

Mabagal hello my website is Mabagal

77 hoki hello my website is 77 hoki

188loto hello my website is 188loto

Lê Lợi hello my website is Lê Lợi

Bagi kalian para pemain slot online yang baru ingin bermain pasti ini menjadi hal yang sulit buat kalian untuk menemukan situs judi slot online terpercaya. Sebenarnya tidak lah sulit menemukan situs game slot online yang cocok untuk kalian, perhatikan lisensi resmi yang di miliki web, semakin banyak situs slot online bekerja sama maka akan semakin terpercaya website tersebut. Juragan69 merupakan pilihan terbaik untuk kalian coba, bekerja sama dengan banyak Lembaga resmi perjudian internasional yang langsung mengawasi sistem fairplay dan data privacy kalian di juragan69 sendiri. Kalian bisa bermain lebih aman dan tenang dan kemenangan kalian pasti akan dibayar oleh juragan69. Dengan perkembangan slot online terpercaya di tahun 2022 akhirnya banyak perusahaan yang membuat begitu banyak permainan slot online yang disukai oleh banyak player. Tidak sedikit game slot online yang sudah ada hingga saat ini, oleh karena itu juragan69 merekomendasikan semua permainan daftar judi slot online bet kecil paling gacor paling banyak dimainkan oleh banyak member di juragan69 :

http://daemin.org/bbs/board.php?bo_table=free&wr_id=23805

1st Deposit Bonus: 100% up to $500 paid in $5 increments. Use bonus code ‘PWB500’ Wagering Requirements: There is no rollover. Min Deposit: $20 No Deposit Bonus: Not Available USA Excluded States: New Jersey, Nevada, Delaware and Maryland. 18+. Begambleaware.org T&C’s Apply You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Another type of bonus offers extended by legal online gambling sites is the no-deposit bonus. These offers grant players free credits simply for signing up on their platform. As the name suggests, this kind of bonus does not require a real-money deposit to be activated. If online poker sites were to instantly award poker bonus cash, then players could simply withdraw and earn themselves free cash.

The test cannot determine the amount of drug used or the exact time of use.

The test cannot determine the amount of drug used or the exact time of use.

… [Trackback]

[…] Read More on that Topic: gafic.com/linked-operation-model-232/ […]

Stablecoins are digital currencies whose value closely tracks that of a stable asset, and so their price should remain stable with their live value hardly moving. However, other cryptocurrencies tend to be highly volatile, which means the live price can change by a large amount in a short space of time. This is not an offer or solicitation in any jurisdiction where we are not authorized to do business or where such offer or solicitation would be contrary to the local laws and regulations of that jurisdiction, including, but not limited to persons residing in Australia, Canada, Hong Kong, Japan, Saudi Arabia, Singapore, UK, and the countries of the European Union. Check the latest cryptocurrency prices and market caps before you buy. The table below shows how different cryptocurrencies are performing in real time.

https://gunnerfgec321852.yomoblog.com/26478470/manual-article-review-is-required-for-this-article

The best platform for user experience and features comes down to personal preference. A new investor just getting into crypto may prefer a simple platform without all the bells and whistles that make it easy to buy crypto. An experienced trader, on the other hand, will likely already be adept at navigating complex trading platforms and prefer a broker with advanced tools and features. Bitfinex allows up to 10x leverage trading by providing traders with access to the peer-to-peer funding market. Using multi-party computing we are able to offer fast round-the-clock withdrawals while maintaining our rigorous security standards. Bitfinex offers order books with top tier liquidity, allowing users to easily exchange Bitcoin, Ethereum, EOS, Litecoin, Ripple, NEO and many other digital assets with minimal slippage.

Your enthusiasm for the subject matter radiates through every word of this article; it’s contagious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

Your positivity and enthusiasm are truly infectious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity to your readers.

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

Your blog has quickly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you put into crafting each article. Your dedication to delivering high-quality content is evident, and I look forward to every new post.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

XXX, This is a good website XXX

Mature, This is a good website Mature

Breast, This is a good website Breast

Sex pill, This is a good website Sex pill

Racy, This is a good website Racy

Intimate, This is a good website Intimate

Clitoris, This is a good website Clitoris

Sex, This is a good website Sex

Prostate, This is a good website Prostate

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

Your blog is a true gem in the vast online world. Your consistent delivery of high-quality content is admirable. Thank you for always going above and beyond in providing valuable insights. Keep up the fantastic work!

I wish to express my deep gratitude for this enlightening article. Your distinct perspective and meticulously researched content bring fresh depth to the subject matter. It’s evident that you’ve invested a significant amount of thought into this, and your ability to convey complex ideas in such a clear and understandable manner is truly praiseworthy. Thank you for generously sharing your knowledge and making the learning process so enjoyable.

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

Your blog has quickly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you put into crafting each article. Your dedication to delivering high-quality content is evident, and I look forward to every new post.

I can’t help but be impressed by the way you break down complex concepts into easy-to-digest information. Your writing style is not only informative but also engaging, which makes the learning experience enjoyable and memorable. It’s evident that you have a passion for sharing your knowledge, and I’m grateful for that.

Your passion and dedication to your craft shine brightly through every article. Your positive energy is contagious, and it’s clear you genuinely care about your readers’ experience. Your blog brightens my day!

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

Your blog has quickly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you put into crafting each article. Your dedication to delivering high-quality content is evident, and I look forward to every new post.

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

I must commend your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable way is admirable. You’ve made learning enjoyable and accessible for many, and I appreciate that.

I wish to express my deep gratitude for this enlightening article. Your distinct perspective and meticulously researched content bring fresh depth to the subject matter. It’s evident that you’ve invested a significant amount of thought into this, and your ability to convey complex ideas in such a clear and understandable manner is truly praiseworthy. Thank you for generously sharing your knowledge and making the learning process so enjoyable.

… [Trackback]

[…] Find More to that Topic: gafic.com/linked-operation-model-232/ […]

This article is a real game-changer! Your practical tips and well-thought-out suggestions are incredibly valuable. I can’t wait to put them into action. Thank you for not only sharing your expertise but also making it accessible and easy to implement.

This article resonated with me on a personal level. Your ability to connect with your audience emotionally is commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

Your unique approach to addressing challenging subjects is like a breath of fresh air. Your articles stand out with their clarity and grace, making them a pure joy to read. Your blog has now become my go-to source for insightful content.

Your enthusiasm for the subject matter shines through every word of this article; it’s infectious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

Your unique approach to tackling challenging subjects is a breath of fresh air. Your articles stand out with their clarity and grace, making them a joy to read. Your blog is now my go-to for insightful content.

I just wanted to express how much I’ve learned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s evident that you’re dedicated to providing valuable content.

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

Your blog has quickly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you put into crafting each article. Your dedication to delivering high-quality content is evident, and I look forward to every new post.

Your writing style effortlessly draws me in, and I find it nearly impossible to stop reading until I’ve reached the end of your articles. Your ability to make complex subjects engaging is indeed a rare gift. Thank you for sharing your expertise!

This article resonated with me on a personal level. Your ability to connect with your audience emotionally is commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

Your storytelling abilities are nothing short of incredible. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I can’t wait to see where your next story takes us. Thank you for sharing your experiences in such a captivating way.

I’d like to express my heartfelt appreciation for this insightful article. Your unique perspective and well-researched content bring a fresh depth to the subject matter. It’s evident that you’ve invested considerable thought into this, and your ability to convey complex ideas in such a clear and understandable way is truly commendable. Thank you for sharing your knowledge so generously and making the learning process enjoyable.

Your unique approach to tackling challenging subjects is a breath of fresh air. Your articles stand out with their clarity and grace, making them a joy to read. Your blog is now my go-to for insightful content.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

I’ve found a treasure trove of knowledge in your blog. Your dedication to providing trustworthy information is something to admire. Each visit leaves me more enlightened, and I appreciate your consistent reliability.

Your dedication to sharing knowledge is unmistakable, and your writing style is captivating. Your articles are a pleasure to read, and I consistently come away feeling enriched. Thank you for being a dependable source of inspiration and information.

Your positivity and enthusiasm are truly infectious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity to your readers.

I’m truly impressed by the way you effortlessly distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply grateful.

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

I’ve discovered a treasure trove of knowledge in your blog. Your unwavering dedication to offering trustworthy information is truly commendable. Each visit leaves me more enlightened, and I deeply appreciate your consistent reliability.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

I’d like to express my heartfelt appreciation for this enlightening article. Your distinct perspective and meticulously researched content bring a fresh depth to the subject matter. It’s evident that you’ve invested a great deal of thought into this, and your ability to articulate complex ideas in such a clear and comprehensible manner is truly commendable. Thank you for generously sharing your knowledge and making the process of learning so enjoyable.

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

Your enthusiasm for the subject matter shines through every word of this article; it’s contagious! Your commitment to delivering valuable insights is greatly valued, and I eagerly anticipate more of your captivating content. Keep up the exceptional work!

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

I am continually impressed by your ability to delve into subjects with grace and clarity. Your articles are both informative and enjoyable to read, a rare combination. Your blog is a valuable resource, and I am sincerely grateful for it.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

https://andyo91zw.webdesign96.com/23036736/5-essential-elements-for-business-trip-message

https://august8dcax.p2blogs.com/22885085/not-known-factual-statements-about-massage-coreen

https://dominick6y7va.blognody.com/22815944/the-single-best-strategy-to-use-for-chinese-massage-music

https://tyson8bbzx.glifeblog.com/22816190/fascination-about-korean-massage-near-19002

https://christianp012auq7.bimmwiki.com/user

https://isocialfans.com/story1188921/the-5-second-trick-for-chinese-medicine-cooling-foods

https://griffina8zi7.yomoblog.com/28606301/top-latest-five-chinese-medicine-brain-fog-urban-news

https://remington41738.life3dblog.com/22851177/fascination-about-chinese-medicine-cooling-foods

https://rylan9sd69.win-blog.com/2089883/facts-about-chinese-medicine-for-inflammation-revealed

https://devin3q890.blogolize.com/the-smart-trick-of-chinese-medicine-for-inflammation-that-no-one-is-discussing-62090330

https://edwiny3455.suomiblog.com/chinese-medicine-body-map-no-further-a-mystery-38200938

https://spencerj8371.diowebhost.com/77561391/little-known-facts-about-chinese-medicine-chicago

https://edgarhjhcz.goabroadblog.com/22813778/everything-about-massage-chinese-foot

https://keeganr0w01.blog-a-story.com/2047843/not-known-facts-about-healthy-massage-bangkok

https://charliej3196.dreamyblogs.com/23067956/what-does-chinese-medicine-cupping-mean

https://kylerl6521.ageeksblog.com/22807650/new-step-by-step-map-for-chinese-medicine-bloating

https://zanderwwtpk.blogpostie.com/44788379/korean-massage-near-me-now-open-for-dummies

https://erick02l6n.hyperionwiki.com/335788/top_latest_five_chinese_medicine_brain_fog_urban_news

https://remingtonq577r.bloguetechno.com/korean-massage-spa-nyc-no-further-a-mystery-58051501

https://rylan4ix19.blogdeazar.com/22998122/rumored-buzz-on-chinese-medicine-certificate

https://wavesocialmedia.com/story1162830/how-much-you-need-to-expect-you-ll-pay-for-a-good-girl-legal-massage

https://georgek937mha4.wikiexpression.com/user

https://herbertp530wsp3.bleepblogs.com/profile

https://kamerons1592.blogdun.com/23131291/rumored-buzz-on-chinese-medicine-body-chart

https://andy7cj07.blogscribble.com/22969802/the-basic-principles-of-chinese-medicine-classes

https://eduardo2mk7p.bloginder.com/23168603/chinese-medicine-cooker-for-dummies

https://dallas48a2f.ampblogs.com/top-chinese-medicine-breakfast-secrets-59141216

https://7prbookmarks.com/story15895551/massage-koreatown-los-angeles-for-dummies

https://johni158eow3.onzeblog.com/profile

https://trevor12g4e.blogars.com/22805219/what-does-chinese-medicine-clinic-mean

https://jeffrey70011.blognody.com/22787534/the-single-best-strategy-to-use-for-healthy-massage-spa

https://bookmarkbooth.com/story15897718/the-single-best-strategy-to-use-for-chinese-medicine-blood-pressure

https://beckettnnmjf.59bloggers.com/23025747/5-simple-techniques-for-thailand-massage-bangkok

https://elliots2233.diowebhost.com/77600498/the-ultimate-guide-to-chinese-medicine-classes

https://zion36654.jts-blog.com/22865561/how-chinese-medicine-chicago-can-save-you-time-stress-and-money

Абузоустойчивый VPS

Виртуальные серверы VPS/VDS: Путь к Успешному Бизнесу

В мире современных технологий и онлайн-бизнеса важно иметь надежную инфраструктуру для развития проектов и обеспечения безопасности данных. В этой статье мы рассмотрим, почему виртуальные серверы VPS/VDS, предлагаемые по стартовой цене всего 13 рублей, являются ключом к успеху в современном бизнесе

http://withoutprescription.guru/# buy prescription drugs online legally

viagra without doctor prescription: non prescription ed pills – best ed pills non prescription

cheapest ed pills: erection pills – best ed pills non prescription

where can i buy amoxicillin without prec: amoxicillin 500 mg purchase without prescription – how to buy amoxicillin online

http://mexicopharm.shop/# best online pharmacies in mexico

VPS SERVER

Высокоскоростной доступ в Интернет: до 1000 Мбит/с

Скорость подключения к Интернету — еще один важный фактор для успеха вашего проекта. Наши VPS/VDS-серверы, адаптированные как под Windows, так и под Linux, обеспечивают доступ в Интернет со скоростью до 1000 Мбит/с, что гарантирует быструю загрузку веб-страниц и высокую производительность онлайн-приложений на обеих операционных системах.

https://medium.com/@HarrisonMi6361/антивирусное-4bba18e91061

VPS SERVER

Высокоскоростной доступ в Интернет: до 1000 Мбит/с

Скорость подключения к Интернету — еще один важный фактор для успеха вашего проекта. Наши VPS/VDS-серверы, адаптированные как под Windows, так и под Linux, обеспечивают доступ в Интернет со скоростью до 1000 Мбит/с, что гарантирует быструю загрузку веб-страниц и высокую производительность онлайн-приложений на обеих операционных системах.

top online pharmacy india: top online pharmacy india – indian pharmacy

cost propecia prices: order generic propecia without prescription – buying cheap propecia no prescription

https://canadapharm.top/# canadian pharmacy online reviews

Levitra 20 mg for sale Levitra 10 mg best price п»їLevitra price

Cheap Levitra online: Buy Vardenafil 20mg online – Levitra online USA fast

Kamagra 100mg: Kamagra Oral Jelly – Kamagra 100mg price

http://tadalafil.trade/# tadalafil best price

win79

https://edpills.monster/# medicine erectile dysfunction

buy Levitra over the counter Levitra 10 mg best price п»їLevitra price

medication for ed: erectile dysfunction medicines – new ed pills

http://kamagra.team/# Kamagra tablets

tadalafil 100mg online: tadalafil generic over the counter – canadian pharmacy tadalafil 20mg

tadalafil online 10mg: cheap tadalafil tablets – where to buy tadalafil in singapore

http://sildenafil.win/# sildenafil tab 50mg cost

https://edpills.monster/# best ed pill

tadalafil generic over the counter tadalafil cheap tadalafil uk pharmacy

sildenafil 25 mg tablet price: 140 mg sildenafil – sildenafil citrate medication

https://kamagra.team/# buy Kamagra

sildenafil 25 mg mexico sildenafil discount coupon sildenafil 150 mg online

Kamagra 100mg: Kamagra 100mg price – Kamagra tablets

ed drugs: new ed pills – п»їerectile dysfunction medication

generic for amoxicillin: purchase amoxicillin online – amoxicillin 500 mg cost

https://doxycycline.forum/# doxycycline online cheap

buy zithromax 1000 mg online: where to get zithromax over the counter – zithromax 500mg price

buy zithromax 500mg online zithromax z-pak zithromax capsules 250mg

prescription drug prices lisinopril: prescription for lisinopril – buy lisinopril 40 mg online

http://ciprofloxacin.men/# buy cipro online usa

ciprofloxacin 500mg buy online Ciprofloxacin online prescription cipro online no prescription in the usa

ciprofloxacin over the counter: antibiotics cipro – buy cipro

amoxicillin 500mg without prescription: amoxicillin 500 mg cost – amoxicillin 500mg without prescription

https://ciprofloxacin.men/# where to buy cipro online

ciprofloxacin mail online buy ciprofloxacin online ciprofloxacin 500 mg tablet price

100 mg doxycycline: doxycycline brand name canada – doxycycline online no prescription

http://azithromycin.bar/# zithromax 500mg price in india

buy ciprofloxacin over the counter Ciprofloxacin online prescription ciprofloxacin order online

lisinopril 420: drug prices lisinopril – lisinopril 100 mg

doxycycline 100mg online: doxycycline tablets online – doxycycline 20 mg

http://doxycycline.forum/# where can i buy doxycycline no prescription

ciprofloxacin 500mg buy online: cipro ciprofloxacin – buy ciprofloxacin over the counter

doxycycline tablets where to buy Doxycycline 100mg buy online doxycycline 100mg pills

https://lisinopril.auction/# can i order lisinopril over the counter

buying prescription drugs in mexico: mexican medicine – medicine in mexico pharmacies

https://buydrugsonline.top/# reliable mexican pharmacies

no perscription pharmacy cheap drugs online canadian online pharmacies not requiring a prescription

pharmacy canada online: buy prescription drugs online – canadian pharmacy canada

canadian pharmacy service: certified canada pharmacy online – canada drugs reviews

https://buydrugsonline.top/# ed meds online

medications with no prescription: online pharmacy no prescription – canadian pharmacy world

canadian meds: order medication online – my canadian drug store

reputable mexican pharmacies online mexican online pharmacy mexican drugstore online

https://mexicopharmacy.store/# mexico pharmacies prescription drugs

can i buy cheap clomid no prescription: clomid best price – generic clomid tablets

http://claritin.icu/# ventolin discount coupon

paxlovid covid: Buy Paxlovid privately – Paxlovid buy online

http://claritin.icu/# buy ventolin pharmacy

how can i get cheap clomid for sale: Buy Clomid Online Without Prescription – how to get clomid without insurance

https://wellbutrin.rest/# purchase wellbutrin in canada

paxlovid pill https://paxlovid.club/# paxlovid for sale

can you buy ventolin over the counter in australia: Ventolin inhaler online – ventolin canada

http://clomid.club/# can i get cheap clomid without insurance

neurontin 400 mg capsules: cheap gabapentin – neurontin 400 mg price

https://paxlovid.club/# paxlovid cost without insurance

b52 club

http://wellbutrin.rest/# generic for wellbutrin xl

neurontin 300 mg cost: generic gabapentin – neurontin capsules 100mg

https://paxlovid.club/# Paxlovid buy online

viagra naturale in farmacia senza ricetta: viagra consegna in 24 ore pagamento alla consegna – kamagra senza ricetta in farmacia

https://avanafilit.icu/# farmacie online autorizzate elenco

acquisto farmaci con ricetta Farmacie a milano che vendono cialis senza ricetta comprare farmaci online con ricetta

farmacia online più conveniente: comprare avanafil senza ricetta – farmacie on line spedizione gratuita

farmacie on line spedizione gratuita: Tadalafil prezzo – farmacia online miglior prezzo

dove acquistare viagra in modo sicuro: viagra online siti sicuri – gel per erezione in farmacia

https://kamagrait.club/# п»їfarmacia online migliore

farmacie online sicure: farmacia online miglior prezzo – farmacia online

b52

Tiêu đề: “B52 Club – Trải nghiệm Game Đánh Bài Trực Tuyến Tuyệt Vời”

B52 Club là một cổng game phổ biến trong cộng đồng trực tuyến, đưa người chơi vào thế giới hấp dẫn với nhiều yếu tố quan trọng đã giúp trò chơi trở nên nổi tiếng và thu hút đông đảo người tham gia.

1. Bảo mật và An toàn

B52 Club đặt sự bảo mật và an toàn lên hàng đầu. Trang web đảm bảo bảo vệ thông tin người dùng, tiền tệ và dữ liệu cá nhân bằng cách sử dụng biện pháp bảo mật mạnh mẽ. Chứng chỉ SSL đảm bảo việc mã hóa thông tin, cùng với việc được cấp phép bởi các tổ chức uy tín, tạo nên một môi trường chơi game đáng tin cậy.

2. Đa dạng về Trò chơi

B52 Play nổi tiếng với sự đa dạng trong danh mục trò chơi. Người chơi có thể thưởng thức nhiều trò chơi đánh bài phổ biến như baccarat, blackjack, poker, và nhiều trò chơi đánh bài cá nhân khác. Điều này tạo ra sự đa dạng và hứng thú cho mọi người chơi.

3. Hỗ trợ Khách hàng Chuyên Nghiệp

B52 Club tự hào với đội ngũ hỗ trợ khách hàng chuyên nghiệp, tận tâm và hiệu quả. Người chơi có thể liên hệ thông qua các kênh như chat trực tuyến, email, điện thoại, hoặc mạng xã hội. Vấn đề kỹ thuật, tài khoản hay bất kỳ thắc mắc nào đều được giải quyết nhanh chóng.

4. Phương Thức Thanh Toán An Toàn

B52 Club cung cấp nhiều phương thức thanh toán để đảm bảo người chơi có thể dễ dàng nạp và rút tiền một cách an toàn và thuận tiện. Quy trình thanh toán được thiết kế để mang lại trải nghiệm đơn giản và hiệu quả cho người chơi.

5. Chính Sách Thưởng và Ưu Đãi Hấp Dẫn

Khi đánh giá một cổng game B52, chính sách thưởng và ưu đãi luôn được chú ý. B52 Club không chỉ mang đến những chính sách thưởng hấp dẫn mà còn cam kết đối xử công bằng và minh bạch đối với người chơi. Điều này giúp thu hút và giữ chân người chơi trên thương trường game đánh bài trực tuyến.

Hướng Dẫn Tải và Cài Đặt

Để tham gia vào B52 Club, người chơi có thể tải file APK cho hệ điều hành Android hoặc iOS theo hướng dẫn chi tiết trên trang web. Quy trình đơn giản và thuận tiện giúp người chơi nhanh chóng trải nghiệm trò chơi.

Với những ưu điểm vượt trội như vậy, B52 Club không chỉ là nơi giải trí tuyệt vời mà còn là điểm đến lý tưởng cho những người yêu thích thách thức và may mắn.

viagra naturale in farmacia senza ricetta viagra online spedizione gratuita pillole per erezione immediata

farmacie on line spedizione gratuita: kamagra gold – farmacia online

farmacie online affidabili: kamagra gel – farmacia online senza ricetta

farmacia online più conveniente: Farmacie a milano che vendono cialis senza ricetta – farmacie on line spedizione gratuita

comprare farmaci online con ricetta farmacia online migliore farmacia online migliore

È il nostro spazio di approfondimento dedicato all’ informazione, per supportarti ogni giorno con i consigli dei nostri farmacisti ed esperti su moltissimi argomenti tra cui Salute e Benessere, Beauty, Mamma e Bambino, Sport, Sostenibilità, Cucina, nutrizione e viaggi. Quando parliamo di Viagra o dei “colleghi” Cialis e Levitra (in un altra occasione ci soffermeremo sulle loro differenza..), parliamo di una categoria di farmaci vasoattivi dal non facile nome scientifico di “inibitori delle fosfodiesterasi”. Fondamentalmente si tratta di farmaci che agendo a livello dei vasi sanguigni dei corpi cavernosi del pene ne agevolano il riempimento e quindi il turgore che determina l’erezione. In particolare agiscono potenziando l’azione di un neurotrasmettitore che si chiama ‘ossido nitrico’ e che viene rilasciato dall’endotelio vascolare e dalle terminazioni nervose durante l’eccitazione sessuale, provocando la dilatazione delle arterie.

http://id.kaywa.com/viagranaturaleabased

Integratore alimentare erboristico in compresse da deglutire. OPERAIO GENERICO La risorsa inserita si occuperà della fissazione di rivetti per il montaggio delle celle frigorifere ed è previsto un percorso di crescita volto alla specializzazione della persona inserita con responsabilit&agra… Scopri come contattarci cliccando qui. Number of characters at least are 3 (necessari solo se diversi dai dati di fatturazione) Bunf propone outfit Uomo e Donna per ogni occasione. Inserisci una data valida (ISO). (necessari solo se diversi dai dati di fatturazione) Lunedì – Sabato: 9:00 – 13:00 e 16:00 – 19:00 Il prezzo per una spedizione mobili in Italia parte da 40 € e può arrivare ad alcune centinaia di euro in caso di traslochi completi di casa o ufficio. Ecco un esempio reale di spedizione mobili su Macingo: mario – un manager che ha cambiato sede di lavoro – per spedire un divano da Roma a Milano, su un tragitto di circa 600 km, ha speso 110 €.

comprare farmaci online all’estero: cialis generico consegna 48 ore – acquistare farmaci senza ricetta

farmacie online sicure: Farmacie che vendono Cialis senza ricetta – farmaci senza ricetta elenco

farmacia online piГ№ conveniente: avanafil prezzo in farmacia – п»їfarmacia online migliore

farmacie on line spedizione gratuita: comprare farmaci online all’estero – farmacia online miglior prezzo

farmacia online piГ№ conveniente avanafil comprare farmaci online all’estero

https://farmaciait.pro/# farmacie online affidabili

farmacie online affidabili: Dove acquistare Cialis online sicuro – farmacia online senza ricetta

viagra naturale: viagra prezzo – viagra online spedizione gratuita

farmacie online sicure: Farmacie che vendono Cialis senza ricetta – farmaci senza ricetta elenco

cerco viagra a buon prezzo: viagra consegna in 24 ore pagamento alla consegna – farmacia senza ricetta recensioni

farmacia online senza ricetta farmacia online piu conveniente п»їfarmacia online migliore

farmacia online miglior prezzo: cialis generico consegna 48 ore – farmacia online senza ricetta

https://sildenafilit.bid/# miglior sito dove acquistare viagra

comprare farmaci online all’estero: avanafil generico – farmaci senza ricetta elenco

farmacia online piГ№ conveniente farmacia online spedizione gratuita migliori farmacie online 2023

top farmacia online: Cialis senza ricetta – acquisto farmaci con ricetta

comprare farmaci online con ricetta: farmacia online più conveniente – acquistare farmaci senza ricetta

acquisto farmaci con ricetta: Farmacie a milano che vendono cialis senza ricetta – farmaci senza ricetta elenco

top farmacia online: cialis prezzo – farmacia online migliore

https://tadalafilit.store/# farmacia online miglior prezzo

farmacia online senza ricetta: comprare avanafil senza ricetta – top farmacia online

farmacie online sicure: kamagra oral jelly consegna 24 ore – top farmacia online

https://tadalafilo.pro/# farmacia 24h

https://vardenafilo.icu/# farmacia online internacional

farmacia online madrid: farmacia online barata – farmacias online seguras en espaГ±a

farmacia online envГo gratis Levitra sin receta farmacias baratas online envГo gratis

http://tadalafilo.pro/# farmacias online seguras en españa

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

Your blog is a true gem in the vast expanse of the online world. Your consistent delivery of high-quality content is truly commendable. Thank you for consistently going above and beyond in providing valuable insights. Keep up the fantastic work!

http://tadalafilo.pro/# farmacia online 24 horas

https://sildenafilo.store/# viagra para hombre precio farmacias

farmacias online seguras: Cialis precio – farmacia online 24 horas

http://kamagraes.site/# farmacia barata

https://vardenafilo.icu/# farmacia 24h

http://kamagraes.site/# farmacia online internacional

https://kamagraes.site/# farmacia barata

sildenafilo 100mg precio espaГ±a: sildenafilo sandoz 100 mg precio – se puede comprar sildenafil sin receta

I’m truly impressed by the way you effortlessly distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply grateful.

I simply wanted to convey how much I’ve gleaned from this article. Your meticulous research and clear explanations make the information accessible to all readers. It’s abundantly clear that you’re committed to providing valuable content.

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

http://kamagraes.site/# farmacia online madrid

farmacia envГos internacionales kamagra 100mg farmacia envГos internacionales

http://sildenafilo.store/# viagra online cerca de bilbao

http://sildenafilo.store/# sildenafilo 50 mg precio sin receta

farmacias online seguras en espaГ±a: farmacias baratas online envГo gratis – farmacia barata

http://sildenafilo.store/# viagra online cerca de bilbao

https://kamagraes.site/# farmacia 24h

Your storytelling prowess is nothing short of extraordinary. Reading this article felt like embarking on an adventure of its own. The vivid descriptions and engaging narrative transported me, and I eagerly await to see where your next story takes us. Thank you for sharing your experiences in such a captivating manner.

https://kamagraes.site/# farmacia online

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

https://kamagraes.site/# farmacia 24h

http://vardenafilo.icu/# farmacia barata

farmacias online seguras: Levitra sin receta – farmacias baratas online envГo gratis

farmacias online baratas Levitra Bayer farmacia online madrid

https://vardenafilo.icu/# farmacia online 24 horas

https://farmacia.best/# farmacia online envÃo gratis

http://kamagraes.site/# farmacias online seguras en españa

farmacia online envГo gratis: farmacia online internacional – farmacia online 24 horas

http://vardenafilo.icu/# farmacias online seguras

https://sildenafilo.store/# sildenafilo 100mg sin receta

farmacia online envГo gratis kamagra gel farmacia online barata

farmacias online baratas: farmacias baratas online envio gratis – farmacias online baratas

http://kamagraes.site/# farmacia envÃos internacionales

http://vardenafilo.icu/# п»їfarmacia online

https://tadalafilo.pro/# farmacias online baratas

comprar viagra en espaГ±a envio urgente comprar viagra en espana comprar viagra sin gastos de envГo

farmacia online 24 horas: vardenafilo sin receta – farmacia online envГo gratis

http://vardenafilo.icu/# farmacia envÃos internacionales

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

http://sildenafilo.store/# viagra para mujeres

http://sildenafilo.store/# sildenafilo cinfa precio

farmacia online barata Precio Levitra En Farmacia farmacia 24h

http://vardenafilo.icu/# farmacias online seguras en españa

farmacia 24h: gran farmacia online – farmacia online internacional

https://tadalafilo.pro/# farmacia 24h

Your blog has rapidly become my trusted source of inspiration and knowledge. I genuinely appreciate the effort you invest in crafting each article. Your dedication to delivering high-quality content is apparent, and I eagerly await every new post.

http://tadalafilo.pro/# farmacias online baratas

http://vardenafilo.icu/# farmacia online

viagra online rГЎpida: viagra generico – sildenafilo 100mg sin receta

http://vardenafilo.icu/# farmacias online seguras

farmacia online internacional farmacia online envio gratis murcia п»їfarmacia online

https://cialissansordonnance.pro/# acheter medicament a l etranger sans ordonnance

pharmacie ouverte 24/24: Levitra pharmacie en ligne – Pharmacie en ligne France

п»їViagra online cerca de Madrid: viagra generico – comprar viagra en espaГ±a envio urgente contrareembolso

In a world where trustworthy information is more crucial than ever, your dedication to research and the provision of reliable content is truly commendable. Your commitment to accuracy and transparency shines through in every post. Thank you for being a beacon of reliability in the online realm.

https://kamagrafr.icu/# Pharmacie en ligne fiable

I’m genuinely impressed by how effortlessly you distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise shines through, and for that, I’m deeply grateful.

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

https://cialissansordonnance.pro/# pharmacie en ligne

п»їViagra sans ordonnance 24h Viagra generique en pharmacie Viagra pas cher livraison rapide france

https://viagrasansordonnance.store/# Viagra pas cher paris

Pharmacie en ligne sans ordonnance: Levitra pharmacie en ligne – Pharmacie en ligne fiable

https://viagrasansordonnance.store/# Meilleur Viagra sans ordonnance 24h

farmacias baratas online envГo gratis: kamagra oral jelly – farmacia barata

https://viagrasansordonnance.store/# Sildénafil 100mg pharmacie en ligne

https://pharmacieenligne.guru/# acheter médicaments à l’étranger

acheter mГ©dicaments Г l’Г©tranger Levitra pharmacie en ligne Pharmacie en ligne livraison gratuite

http://pharmacieenligne.guru/# pharmacie en ligne

Prix du Viagra 100mg en France: Viagra generique en pharmacie – Viagra pas cher paris

farmacia online internacional: Levitra sin receta – farmacia barata

https://kamagrafr.icu/# Pharmacie en ligne France

http://levitrafr.life/# acheter médicaments à l’étranger

http://cialissansordonnance.pro/# Pharmacie en ligne livraison rapide

https://kamagrafr.icu/# Pharmacie en ligne livraison rapide

farmacia online 24 horas: Levitra Bayer – farmacia online envГo gratis

Pharmacie en ligne sans ordonnance: pharmacie en ligne pas cher – Pharmacie en ligne fiable

http://pharmacieenligne.guru/# Pharmacie en ligne France

https://cialissansordonnance.pro/# Pharmacies en ligne certifiées

This article resonated with me on a personal level. Your ability to emotionally connect with your audience is truly commendable. Your words are not only informative but also heartwarming. Thank you for sharing your insights.

I couldn’t agree more with the insightful points you’ve articulated in this article. Your profound knowledge on the subject is evident, and your unique perspective adds an invaluable dimension to the discourse. This is a must-read for anyone interested in this topic.

http://levitrafr.life/# acheter médicaments à l’étranger

pharmacie ouverte 24/24 pharmacie en ligne sans ordonnance Pharmacie en ligne fiable

farmacia envГos internacionales: comprar cialis online seguro opiniones – п»їfarmacia online

https://pharmacieenligne.guru/# Acheter médicaments sans ordonnance sur internet

https://cialiskaufen.pro/# п»їonline apotheke

online apotheke preisvergleich potenzmittel rezeptfrei internet apotheke

I couldn’t agree more with the insightful points you’ve made in this article. Your depth of knowledge on the subject is evident, and your unique perspective adds an invaluable layer to the discussion. This is a must-read for anyone interested in this topic.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

Your positivity and enthusiasm are undeniably contagious! This article brightened my day and left me feeling inspired. Thank you for sharing your uplifting message and spreading positivity among your readers.

http://viagrakaufen.store/# Billig Viagra bestellen ohne Rezept

online apotheke versandkostenfrei potenzmittel online-apotheken

https://potenzmittel.men/# gГјnstige online apotheke

I’m truly impressed by the way you effortlessly distill intricate concepts into easily digestible information. Your writing style not only imparts knowledge but also engages the reader, making the learning experience both enjoyable and memorable. Your passion for sharing your expertise is unmistakable, and for that, I am deeply grateful.

Your passion and dedication to your craft radiate through every article. Your positive energy is infectious, and it’s evident that you genuinely care about your readers’ experience. Your blog brightens my day!

I wanted to take a moment to express my gratitude for the wealth of invaluable information you consistently provide in your articles. Your blog has become my go-to resource, and I consistently emerge with new knowledge and fresh perspectives. I’m eagerly looking forward to continuing my learning journey through your future posts.

versandapotheke versandkostenfrei online apotheke gunstig versandapotheke

https://cialiskaufen.pro/# versandapotheke

https://apotheke.company/# online apotheke gГјnstig

online-apotheken Potenzmittel Schneller Besser versandapotheke versandkostenfrei

https://potenzmittel.men/# internet apotheke

gГјnstige online apotheke: potenzmittel – versandapotheke deutschland

http://apotheke.company/# online apotheke versandkostenfrei

online apotheke versandkostenfrei potenzmittel rezeptfrei versandapotheke deutschland

https://cialiskaufen.pro/# versandapotheke versandkostenfrei

http://mexicanpharmacy.cheap/# mexican rx online

mexico pharmacy mexican rx online mexico drug stores pharmacies

I must applaud your talent for simplifying complex topics. Your ability to convey intricate ideas in such a relatable manner is admirable. You’ve made learning enjoyable and accessible for many, and I deeply appreciate that.

This article is a true game-changer! Your practical tips and well-thought-out suggestions hold incredible value. I’m eagerly anticipating implementing them. Thank you not only for sharing your expertise but also for making it accessible and easy to apply.

medication from mexico pharmacy purple pharmacy mexico price list best online pharmacies in mexico

purple pharmacy mexico price list mexican drugstore online mexican online pharmacies prescription drugs

https://mexicanpharmacy.cheap/# purple pharmacy mexico price list

mexico drug stores pharmacies medicine in mexico pharmacies mexican rx online

https://mexicanpharmacy.cheap/# medicine in mexico pharmacies

best online pharmacies in mexico mexican drugstore online mexico pharmacies prescription drugs

mexican border pharmacies shipping to usa buying prescription drugs in mexico online mexico pharmacy